1. Introduction: Why the AI supply chain matters

The AI supply chain is quickly becoming one of the most powerful drivers of global growth. From chips and data centres to cloud platforms and digital services, every link in this chain shapes which countries and companies will lead in the coming decade.

In 2026, the race is intensifying between the United States, China and the European Union as each one tries to secure its position in this new technological landscape. Understanding how the AI supply chain works is now essential for businesses, investors and policymakers who do not want to be left behind.

2. From idea to infrastructure

Modern artificial intelligence systems rely on three pillars: powerful models, massive data and advanced computing infrastructure. The leap in generative tools over recent years has been possible because all three have advanced together, supported by large investments in hardware and networks.

However, none of this happens in isolation. It depends on a global web of suppliers, technology firms and service providers that turns cutting‑edge research into real‑world applications.

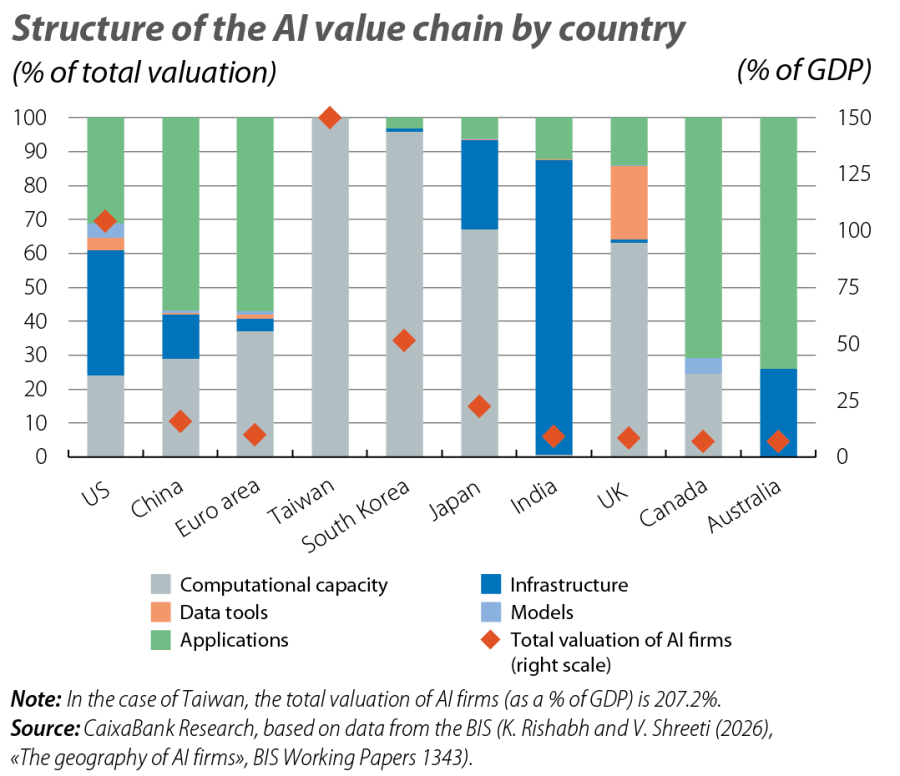

3. The layers of the AI supply chain

At the base of the AI supply chain sit critical minerals used to manufacture sophisticated semiconductors, often called the “physical brain” of modern systems. These chips are then integrated into data centres, communication networks, power grids and cloud services—the “body” that allows huge volumes of data to be processed at scale.

On top of this hardware layer, companies develop foundational models trained on vast datasets, which then support a growing number of applications and digital services. Real economic value is created when these services are adopted by firms and consumers, changing how work is done and how products are delivered.

4. Innovation: the first phase of deployment

The first phase of deployment is the innovation stage, where new models, techniques and breakthrough applications are developed. In this phase, the United States is clearly ahead, leading in top model performance, research output, open‑source projects and chip design activity.

This early leadership gives the US a strong position in setting technical standards and capturing the highest‑value parts of the AI supply chain. It also attracts global talent and investment towards its innovation hubs.

5. Building the backbone: infrastructure investment

The second phase focuses on infrastructure: investing heavily in data centres, chips, transmission networks and energy capacity. Many economies are now experiencing a strong infrastructure boom as they rush to expand their AI supply chain and avoid falling behind rivals.

These investments are highly capital‑intensive and require long‑term planning, especially in areas such as power generation and grid upgrades. Countries that move early can create a durable advantage by offering reliable, large‑scale computing resources to businesses and developers.

6. Diffusion and adoption across economies

Once tools become robust and accessible, they spread across sectors and user groups in the diffusion and adoption phase. Early evidence shows that individuals and firms are adopting these tools faster than they adopted past digital technologies, particularly in advanced economies.

However, adoption is not equal. Some sectors and firms quickly integrate new tools into their workflows, while others experiment slowly or wait on the sidelines, creating gaps in productivity and competitiveness.

7. The US lead and China’s rapid catch‑up

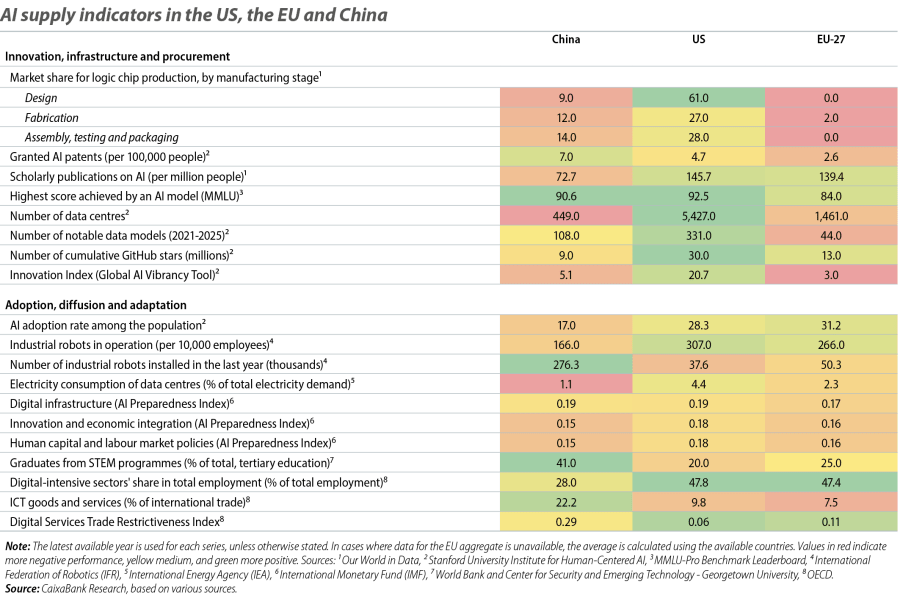

In terms of innovation and infrastructure, the US still holds a clear lead, but China has shown a striking ability to catch up with the technological frontier. The most advanced Chinese models now perform at a very similar level to their American counterparts, supported by a surge in patents, aggressive investment and a strong push to upgrade its industrial base.

For the AI supply chain, this means we are moving towards a world with at least two powerful hubs rather than a single dominant centre. Companies and governments must now think carefully about standards, interoperability and how exposure to each hub affects their long‑term strategy.

8. Europe’s weaker position in chips

The European Union is less well positioned on the innovation side of the AI supply chain than the US and China. Its relatively low market share in chip production leaves it heavily dependent on external suppliers and also behind in foundational model development, even though it has strong research institutions and digital service firms.

This gap in hardware and models creates a strategic vulnerability, because the region risks becoming a “rule‑maker but not a tool‑maker” in the global ecosystem. To close this gap, Europe will need sustained investment in semiconductors, computing infrastructure and skills, while maintaining its strength in regulation and trust.

9. China’s strength in critical materials

China has a decisive advantage in the supply of materials, thanks to its access to critical minerals and its strong processing capacity for chips and semiconductors. This central position in the early stages of the AI supply chain gives it leverage over key inputs that other countries need to keep expanding their own infrastructure.

At the same time, China is using this position to support a rapid modernisation and robotisation of its manufacturing sector. By combining control over inputs with large‑scale deployment in factories and services, it aims to become not only a supplier but also a major user and exporter of advanced solutions.

10. Bottlenecks in chips, data centres and energy

Despite the surge in investment, there are serious bottlenecks in the chip market, in available data centre capacity and in energy supply. These constraints could slow down deployment and increase tensions between countries competing for the same strategic resources, especially where export controls and industrial policy collide.

Model capabilities are improving at an exponential pace, with new systems able to handle much longer and more complex tasks than those available just a year ago. If infrastructure and energy do not keep up with this progress, the AI supply chain could face recurring shortages and higher costs, making long‑term planning harder for both firms and policymakers.

11. A long race with global consequences

The development of the AI supply chain is a long‑distance race rather than a short sprint. How the US, China, Europe and other regions manage innovation, infrastructure, resources and regulation will shape not just future growth, but also the global balance of power and the way technologies are governed.

For businesses, the message is clear: understanding this supply side is now a strategic necessity, not a niche concern. Those that plan for different scenarios, diversify their exposure and invest early in skills and complementary technologies will be best placed to benefit as this new wave of transformation unfolds.